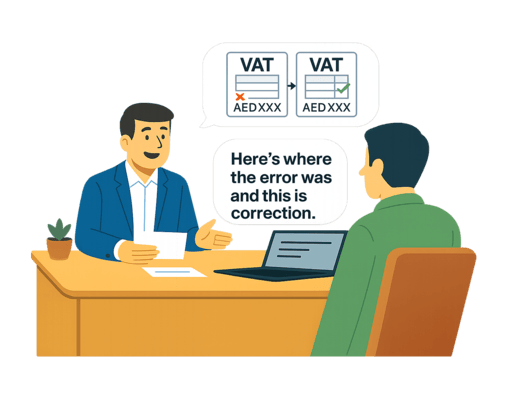

In simple terms : It’s a formal notification to the FTA (Form 211) that corrects an error or omission in a VAT return, refund claim, or assessment so you can fix liability and limit penalties.

Claim compliance certainty. Limit penalties. File Form 211 correctly.KWS provides an end-to-end VAT voluntary disclosure service for businesses across Dubai and the UAE — from eligibility checks and Form 211 preparation to portal submission and post-submission follow-up.

The FTA VAT Voluntary Disclosure UAE is a formal mechanism that allows a taxable business to proactively correct errors or omissions in previously submitted tax records. This form, commonly known as VAT211, is provided by the Federal Tax Authority (FTA).

The Taxpayer uses this formal process to officially notify the FTA of an error or mistake found in a previously filed:

Filing voluntarily demonstrates good faith, corrects under‑reported tax or incorrect refunds, and typically reduces enforcement exposure compared with errors discovered by the FTA later. Because when the FTA finds the error first the penalties are often significantly higher, early disclosure reduces financial and compliance risk.

| What We Do | Why It Matters |

|---|---|

| Eligibility review and scoped liability calculation | Ensures you disclose only what’s necessary |

| Drafting of Form 211 and supporting narrative (English) | Structured to meet FTA expectation |

| Document checklist and file preparation | Reduces chances of follow-up requests |

| Submission via the FTA e-Services portal | Official filing channel for disclosures |

| Post-submission tracking and FTA follow-up | Speeds resolution and clarifies penalties |

Form 211 is the official route for voluntary corrections. If your corrected liability exceeds AED 10,000,you must filewithin 20 business days of discovering the error. Even for smaller differentials, act promptly to limit exposure. KWS will prioritise and prepare your case pack as soon as you instruct us.

We quantify the error, identify affected tax periods, and confirm whether Form 211 is required.

We calculate corrected VAT liability, interest, and an initial penalty estimate.

We prepare the disclosure, a concise factual narrative, and the supporting evidence required by the FTA.

You review the case pack; we finalise the filing for submission.

We submit via the FTA e-Services portal and track the case until closure, handling FTA queries on your behalf.

| Item | When required |

|---|---|

| Original VAT returns and revised computations | Always |

| Sales and purchase invoices | To support corrections |

| Bank statements and payment evidence | For reconciliations |

| Contracts or agreements (if relevant) | For specific transactions |

| Covering letter / factual narrative | Explains cause and corrective steps |

KWS validates computations and document completeness before filing to minimise rework.

A voluntary disclosure does not automatically remove penalties, but timely and complete disclosures are favourably considered and generally reduce enforcement action compared with issues identified by the FTA. Exact penalty treatment depends on facts, materiality, and FTA discretion.

KWS verifies calculations and document completeness to reduce the risk of follow-up queries.

A retail client discovered a reporting gap across three quarterly returns that increased VAT due by AED 28,000. KWS performed an eligibility check, prepared Form 211 and supporting reconciliations, submitted the disclosure, and negotiated a materially reduced penalty outcome compared with enforcement discovery.

FAQs

KWS offers a comprehensive suite of services, including accounting, payroll processing, tax preparation, financial advisory, and global payroll solutions.

A formal correction filed to the FTA using Form 211 to notify and rectify an error in previous VAT filings.

If the differential amount exceeds AED 10,000, file within 20 business days of discovery. For lower differentials, disclose promptly and seek guidance.

Missing the window increases the risk that the FTA will treat the matter as non-voluntary, which can lead to higher penalties and enforcement action. KWS can advise on remedial steps and represent you in communications with the FTA.

Yes — foreign entities with UAE VAT obligations should file disclosures when they identify errors.

Processing time varies with complexity and evidence provided. KWS tracks the case and follows up until resolution.

Effortlessly handle VAT Voluntary Disclosure with KWS’s expert services.

VAT Voluntary Disclosure in UAE

Free eligibility scan before submission

No hidden fees

Starts From

Get a fast eligibility check and a clear, costed path to file Form 211.